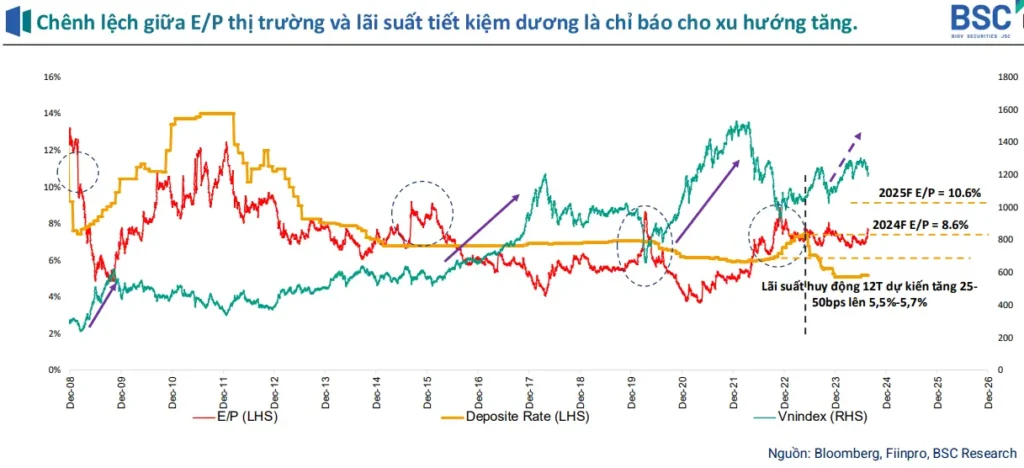

Comparing market profitability and savings interest rates, BSC finds necessary and sufficient conditions for forming a medium and long-term growth trend.

The market has established an uptrend.

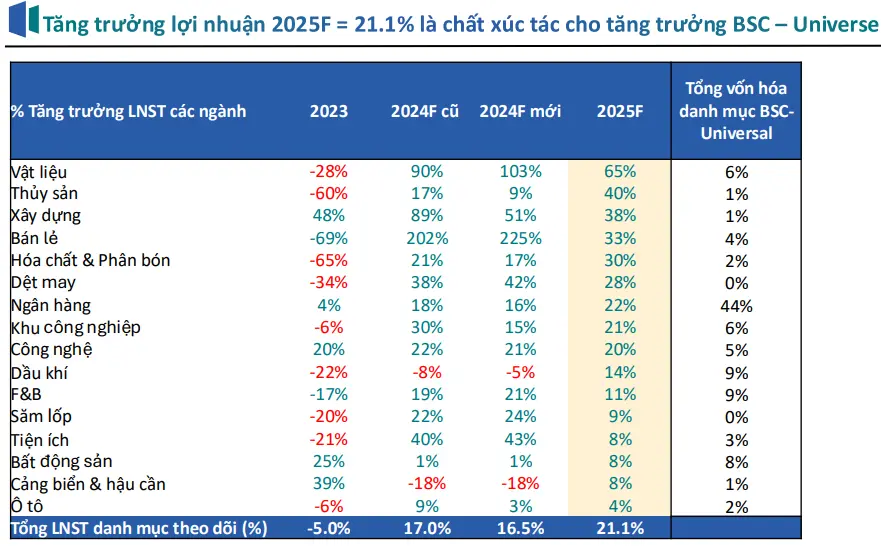

In a recent report, BSC Securities estimated that the growth in net profit after tax - equity (NPATMI) of the whole market recorded a growth of 20%, led by the non-financial sector group of +34% compared to the same period, recording the third consecutive quarter of positive growth and affirming the recovery trend of the economy.

Looking at the second half of the year, BSC slightly adjusted down the BSC-Universe growth forecast for 2024 from 17% to 16.5% mainly due to downward adjustments in the forecast for the banking, industrial park, construction, chemical-fertilizer and seafood groups, while increasing the forecast for the retail group Retail, Construction Materials, Textiles, F&B.

BSC assesses that with the exchange rate pressure expected to cool down as the Fed cuts interest rates, profit growth in the second half of the year will continue to be supported mainly by lower interest expenses, reduced exchange rate losses, reduced sales and business management costs, along with a low base level in Q3/2023. Therefore, the risk of forecasting lower-than-market profit growth as in Q3/2023 will be minimized.

Compare market returns and savings interest rates

Comparing the market's profitability and savings interest rates, which are considered reputable indicators of market trends, BSC found that the necessary conditions for the formation of a medium- and long-term market growth trend come from (1) The profitability of the stock market is more attractive than other investment channels, and the sufficient condition is (2) EPS maintains an increasing rate to ensure that the expected profitability continues to maintain an attractive level, similar to what happened in 2015-2016 and 2020-2021.

“Therefore, in the context of projected profit growth in 2025 = 21.1% YoY, we expect the market to maintain an upward trend in the remaining period of 2024 and 2025,” the BSC report stated.

BSC believes that in the context of low interest rates, the EPS growth rate of enterprises will be the main driving force for stock prices with E/P fwd 2024 VN-Index = 8.6% and at the end of 2025 = 10.6%, higher than the current interest rate of ~5.5-6%.

Attractive market valuation

At PE trailing = 13.4x and PB trailing = 1.5x, after updating Q2/2024 business results and the strong market correction in the first half of Q3/2024, VN-Index is trading at an attractive valuation compared to history, only about 5% -6% higher than the historical bottom of Q2/2020 (Covid pandemic), Q4/2022 (Van Thinh Phat) and Q3/2023 (strong market correction when Q3 business results grew worse than market expectations).

With the assessment that market profits will continue to improve in the second half of the year and the market has a relative discount, -6.5% compared to the peak in 2024, BSC believes that the corrections are a good opportunity to accumulate stocks for the medium and long term, investors can choose the strategy of buying "spreading nails" at attractive price zones.

Regarding valuation, BSC believes that the gap between valuations of non-financial sectors (excluding Banking, Real Estate, Securities) is gradually narrowing after the strong correction in July 2024 and the strong profit growth of this sector. PE FWD 2024 of BSC-Universal's non-financial sector is at 15.3 times, approaching the standard deviation of -1 time and lower than the 5-year average of 18 times.

Therefore, BSC believes that the downside risk will be limited and the correction will be more of an opportunity than a risk. However, it is also necessary to note that the risks mentioned above related to the risk of recession will be able to affect the profit growth rate as well as the valuation forecast.

Source: CafeF